Authored By: Diksha Pandey

Micro, Small and Medium-sized Enterprises (MSMEs) are set to play a crucial role in India’s transformation into an outward-looking global economy. Contributing close to 30% to our GDP, and employing over 120 million people [1], MSMEs have the potential to de-burden the agricultural sector and help in the diversification of the country’s economic landscape. While MSMEs are generally considered to be flexible in adapting to new developments in the economy, most find it difficult to grow into large companies [2].

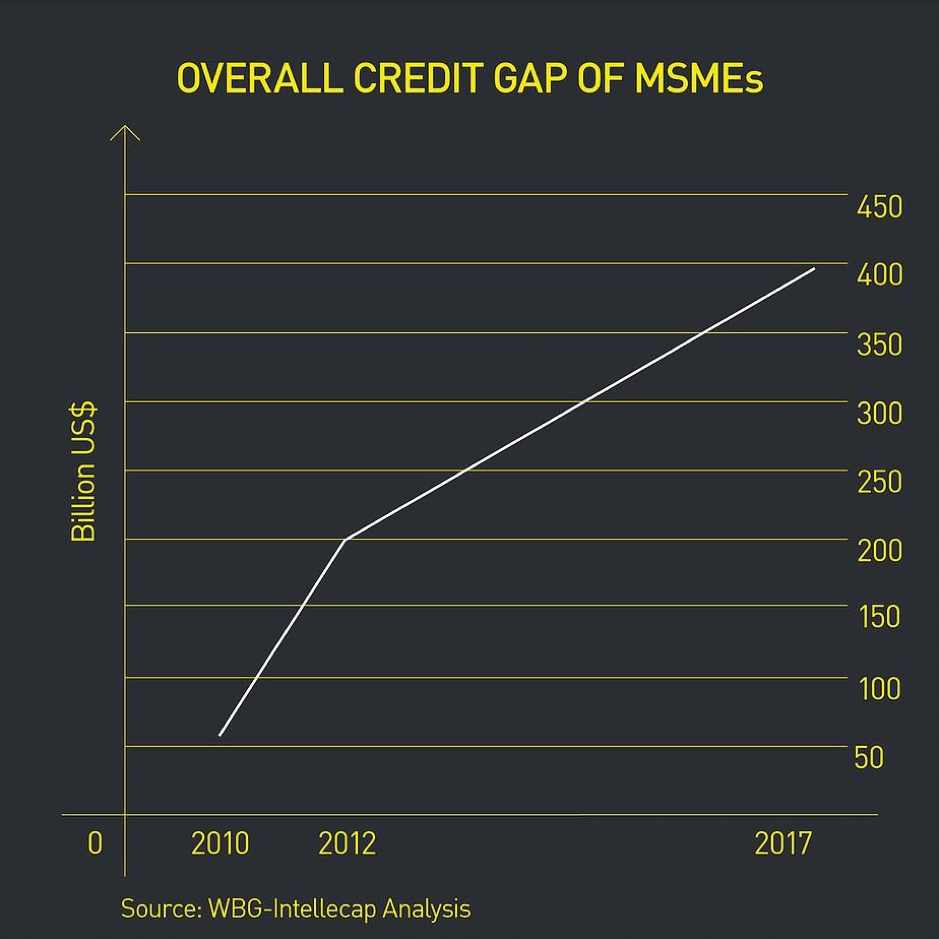

One of the major causes for this limitation is that small firms lack access to formal sources of external finance. To quantify the magnitude of the problem, the 60 million enterprises that constitute this sector collectively face a credit shortage of over 300 billion USD, while the total government spending stands at 400 billion USD. In the above context, the paper explores how technological disruptions in the financial services industry are taking care of this particular growth constraint by providing access to “instant, automated, and remote” credit [3].

BARRIERS TO ACCESSING FINANCE

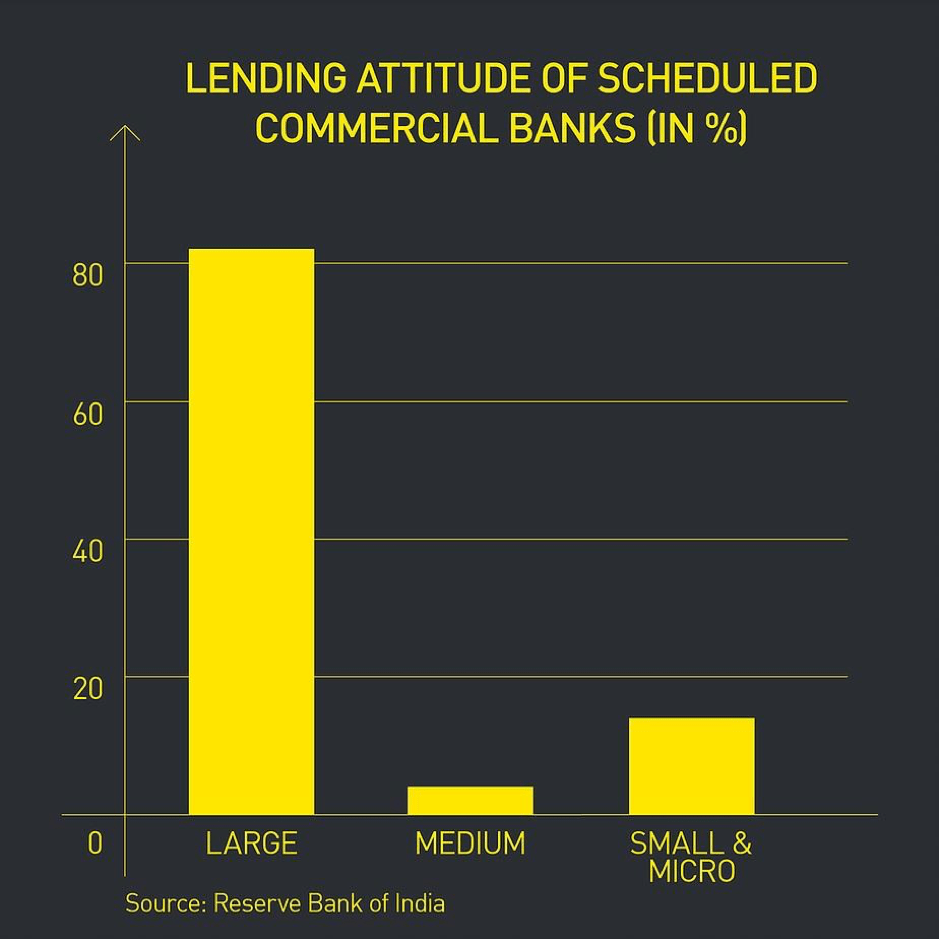

During the financial year of 2017-2018, scheduled commercial banks [4] lent out less than 20% of their total resources to minor establishments. There are many explanations for why India’s legacy banks dominated financial market has not been very accommodating of informal small-ticket businesses. For instance, banks are discouraged by the rarity of long-standing relationships with MSMEs given their short life cycle, as opposed to big established businesses, rendering any association unprofitable [5]. The size of loans and the size of firms have a direct linear correlation, and the administrative cost of lending out small loans is higher.

It has not been favourable for banks to restructure loans given out to MSMEs in cases of default based on genuine reasons, indicating that the monetary environment isn’t flexible enough to support the growth of MSMEs. Tedious documentation processes, registration status and geographical location of the firm, level of education and gender of the owner, as well as bank penetration levels are also suspected to impact access [6].

Further, exploring the demand side constraints, MSMEs find themselves unable to paint a clear picture of their financial standing. Due to lack of resources and expertise, as well as financial illiteracy, MSMEs often do not maintain audited accounts and formal transactional histories [7]. There is also the problem of foreclosing sufficient assets as collateral. This translates into traditional lenders finding it difficult to verify the creditworthiness of these businesses, making it high-risk lending.

However, it is possible that the risk factor associated with lending to MSMEs might be overstated. Analysing the Non-Performing Asset (NPA) crisis along the criteria of the size of firms, big businesses account for most of the bad loans. Their share has, concurrently, shown an increasing trend, as opposed to a more consistent record of small businesses.

As a result of the above, MSMEs are forced to be heavily reliant on the informal sector for just about 900 billion USD [8], which are all unsecured loans, however, offered at comparatively higher interest rates.

To reduce this dependency on the unorganised lending sector, the government launched the MUDRA Scheme to provide microfinance to small businesses. Even though the number of loans sanctioned and disbursed, as well as the number of accounts opened, under the scheme have increased exponentially since the launch of the scheme in 2015, a singular reliance on MUDRA finance for meeting the addressable credit demand of MSMEs will be tricky.

Furthermore, the MUDRA loans are without collateral, which, while making it easy to avail the loans, also contributes to the rising NPA problem. Monetary decision-makers in the country are aware of the problem, and very recently, the Reserve Bank of India proposed the creation of a stressed asset fund for the resolution of the same. Coupled with this, the size of loans given out under PMMY averages at ₹ 44,500 [9]. This amount has been deemed to be insufficient to start a business that can generate employment. Subsequently, loans exceeding 5 lakhs constitute merely 1.3 per cent of the total loans given out [10], indicating that the focus has remained restricted to increasing the number of loans disbursed rather than increasing the amount of credit made available to every borrower, forcing a borrower to depend on multiple lenders.

DIGITAL, ACCESSIBLE AND CHEAP

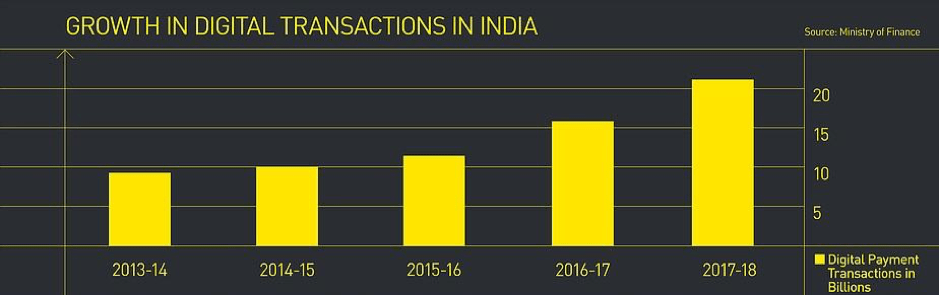

A viable solution to fix the credit deficiency of MSMEs lies in the processes of digitalisation. The intended scope of the ongoing global technological revolution has evolved beyond the primary target of expanding broadband coverage, to a more advanced objective of moving all major monetary exchanges to online platforms. This has prompted the rise of several FinTech innovators and B2B lending start-ups which are ushering in a new age of alternative lending sources, to serve the previously underserved population in both developed and developing countries.

Technological advances in the field of blockchain, virtual currencies, biometrics, and data analytics have altered the demand and expanded the use of collateral. FinTech companies are also reaching out to government agencies, including PSBs, MFIs and NBFCs, in an effort to develop a partnership focusing on better implementation of the MUDRA scheme.

It is easy to understand why going digital will be a vital step taken for correcting the credit shortfall faced by MSMEs. Data-intensive digital financing has not only lowered the cost of reaching out to small, and potentially risky, clients, but underwriting decisions are also now easier to make. Advances in AI technology has allowed a digital footprint, as a non-traditional source of information, to be used in developing reliable credit scores for MSMEs. Mobile history, including contact lists, and tracking online activities such as credit card payments, are being used to determine the cash flow of businesses and assess repayment capacity and lending risks.

Services such as e-KYC, e-Sign, UPI, and Digital Locker have significantly reduced the turnaround time for loans. The credit secured through digital financiers is also cheaper, as the structural and operational costs are reduced. The fact that most MSMEs switching to these alternative lenders are New-To-Credit borrowers also creates a level playing field, eliminating harmful competition over limited resources.

WAY FORWARD

The advantages are many, and digital tech is expected to clout $2 trillion of global economic output by 2020 [11]. Furthermore, the set of technologies that directly impact the financial services industry is expanding rapidly. However, digital maturity does not come naturally to Indian borrowers; it needs to be instilled and nurtured.

There also exist several caution points. We need to be wary of any possible exaggerations regarding the cost advantage of digital finance, as expanding internet coverage in itself is a costly affair, let alone ensuring the quality of connectivity. A major challenge for the venture capital industry in India is to evolve beyond the ‘friends and family’ network and ensure inclusivity. The country will also need to be careful to avoid monopolistic trends in digital infrastructure, as is being observed with PayPal dominating over 90% of the market share in the United States [12]. How the entry of large tech companies in the market to finance small businesses will impact the incumbent players will also need to be studied more extensively. Giving an insight into the same, Manish Lunia, co-founder of FlexiLoans, a DigiTech start-up, says:

“We allow people with poor CIBIL scores to increase their business. If the business does well, why would they default? With a healthy business growth, one is more likely to repay and improve his CIBIL score. This will help them take big ticket-size loans from banks in the future”

The journey of MSMEs, from having an online presence, to adapting e-payments, e-commerce, and finally e-banking, will only be fast-tracked by innovative policy interventions. In the past few years, the Indian government has been consistently working towards the dream of a cashless, digital India. Demonetisation, JAM Trinity, and the introduction of the GST have all propelled digitalisation and formalisation of individuals and businesses alike, thereby promoting last-mile connectivity.

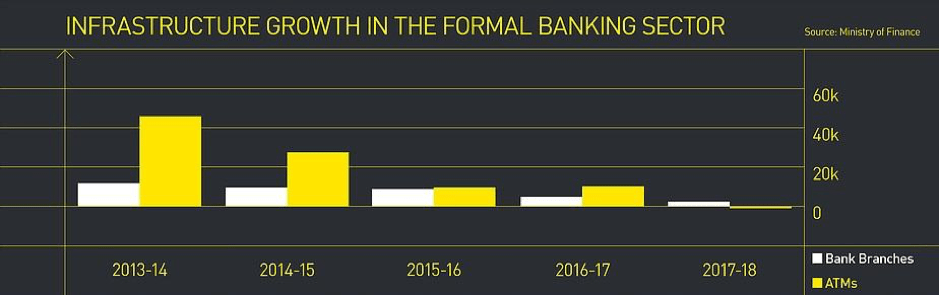

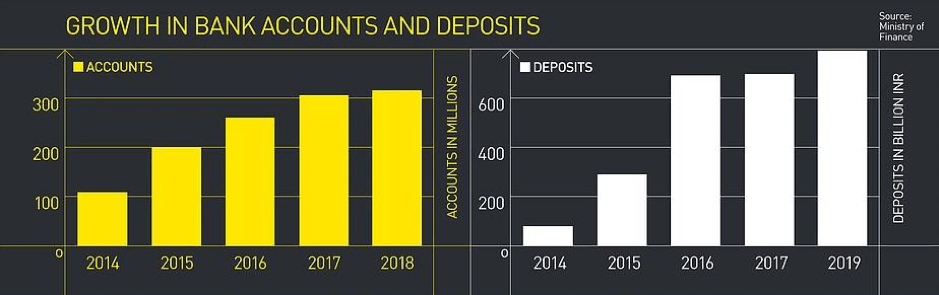

However, special efforts are required to ensure that the momentum of digital movement in India does not slow down, as is being indicated by a nominal increase in the number of basic savings banking accounts, as well as deposits made in the same from 2016 to 2018. The expansion of formal banking infrastructure, while initially propelled with great force, is also showing worrisome trends of deceleration.

A lot more can be done to fully exploit the fact that return on FinTech investments is estimated to be the highest in India at 29%, against the global average of 20% [13]. To converge the goal of digital empowerment with economic mobility and financial inclusion will be a good place to start.

ENDNOTES

[1]https://www.cii.in/Sectors.aspx?enc=prvePUj2bdMtgTmvPwvisYH+5EnGjyGXO9hLECvTuNuXK6QP3tp4gPGuPr/xpT2f

[2] https://www.oecd.org/sti/ind/Policy-Note-No-Country-For-Young-Firms.pdf

[3] http:// www.cgap.org/blog/instant-automated-remote-keyattributes-digital-credit

[4] Scheduled commercial banks are those banks which are included in the Schedule II of RBI Act, 1934. Scheduled commercial banks carry out the normal business of banking activities such as accepting deposits, giving loans and other banking services

[5] https://www.diw.de/documents/publikationen/73/diw_01.c.42833.de/dp469.pdf

[6] https://www.ifc.org/wps/wcm/connect/a2aef7a2-6d46-433c-ab02-06cd00591cea/121264-WP-PUBLIC-MSMEReportFINAL.pdf?MOD=AJPERES

[7] https://www.ifc.org/wps/wcm/connect/409734804c561178926edaf12db12449/TOS_SME.pdf

[8] http://documents.worldbank.org/curated/en/386141468331458415/pdf/713150WP0Box370rillion0and0counting.pdf

[9] https://www.mudra.org.in/

[10] https://www.indiatoday.in/india/story/mudra-yojana-is-a-mission-or-mess-5-point-fact-checker-1244538-2018-05-29

[11] https://www.accenture.com/_acnmedia/PDF-14/Accenture-Strategy-Digital-Disruption-Growth-Multiplier-Brazil.pdf

[12] https://financesonline.com/legit-payment-gateway-providers-usa/

[13] https://www.pwc.in/assets/pdfs/publications/2017/fintech-india-report-2017.pdf