Introduction

In 2025, India experienced extreme weather events on 99% of the days from January to September, resulting in over 4,000 deaths, with heavy rains, floods and landslides accounting for the majority of these fatalities (Down to Earth, 2025). The recent floods in Punjab have affected nearly 20 lakh people with more than 3 lakh individuals displaced from their homes. The latest cloudburst incident in Uttarakhand, which triggered landslides and floods, has been reported to have caused significant damage to the infrastructure and agriculture of the region, with losses reaching millions.

Hazards, especially natural ones, are the major drivers of disasters, resulting in human displacement and economic losses. Not all hazards and corresponding disasters are the same. Hazards such as Cyclones can be forecasted and prepared for, while others, such as drought, develop slowly and their disastrous nature is often revealed much later than their onset, and usually too late to mitigate against. Other hazards, such as earthquakes, strike with little to no warning, and the only way to mitigate against them is to learn from the impacts of past events.

According to Global Assessment Report (GAR) on Disaster Risk Reduction 2025, in the last 25 years, over 10,000 natural hazards and disasters have been recorded globally, costing trillions of dollars to the global economy and affecting nearly half the world’s population. The disastrous Yangtze River Flood in China in 1931, the Great Bhola Cyclone in Bangladesh in 1970, the Bhuj Earthquake in India in 2001, and the recent Wildfires in the USA have made a significant mark in history for the damage they caused.

India, with a landmass of over 3.2 million km², has nearly two-thirds of its states and union territories prone to disasters, as a significant portion of the country’s land and coastline is highly vulnerable (NDMA AR2021-22). Although India has recently risen to become the fourth-largest economy in the world, its per capita GDP remains below 3,000 USD, making the country particularly vulnerable to the severe economic impacts of natural hazards. Another side of disasters is large-scale human displacement, often forcing vulnerable populations into cycles of poverty and migration. Post-2008, India has emerged as one of the top countries globally in terms of internal displacement caused by natural hazards as per the Internal Displacement Monitoring Centre (IDMC).

This raises an urgent question: how prepared is India to protect both its economy and its people from disasters caused by natural hazards?

What does the Data on Loss and Damage Say?

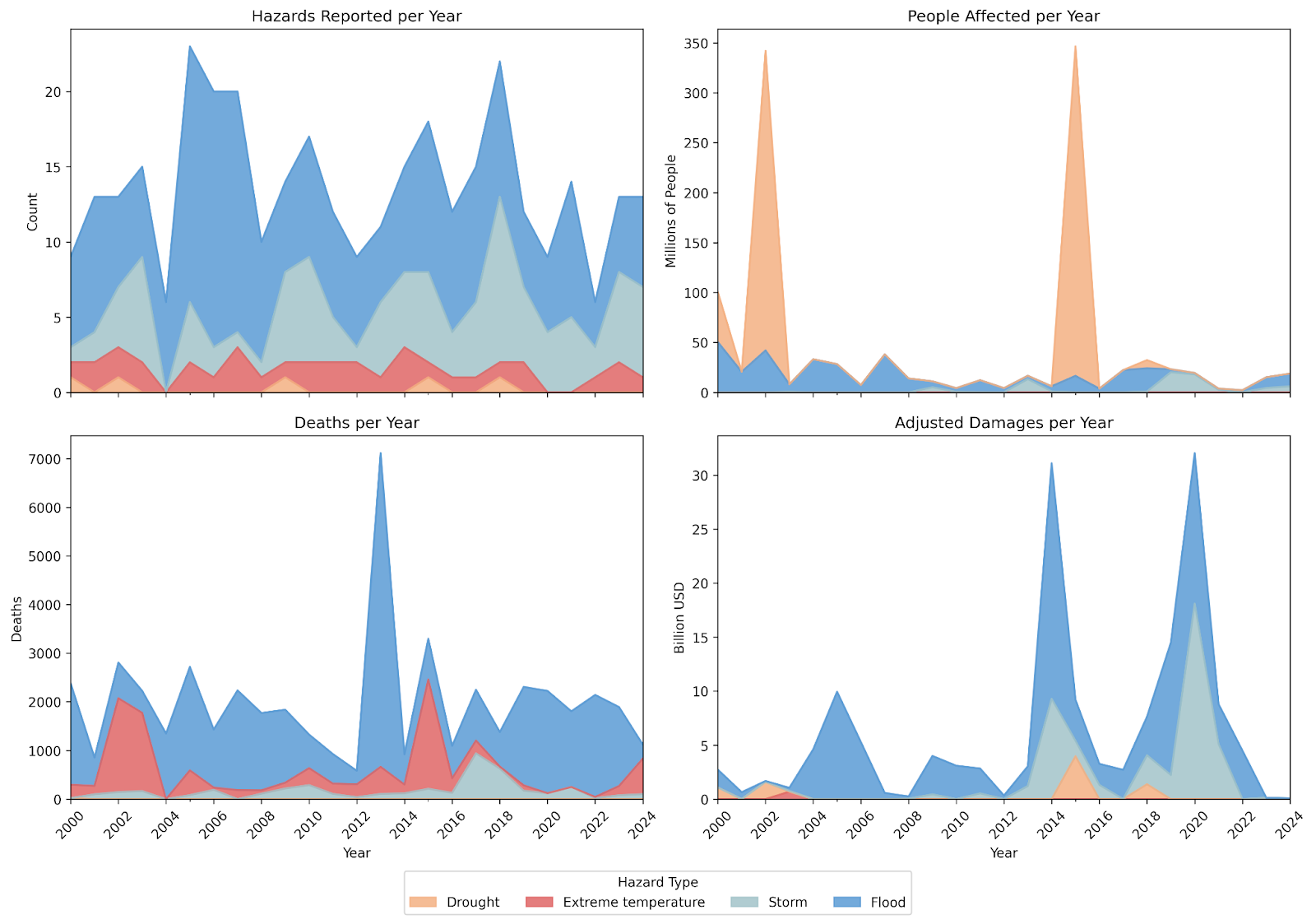

We analysed the Emergency Events Database (EM-DAT) data for India (Figure 1). According to EM-DAT, between 2000 and 2024, India reported nearly 400 disasters caused by natural hazards, resulting in an estimated total damage of over USD 162 billion, which affected millions and led to permanent or temporary displacement (EM-DAT).

Floods are the most frequent and destructive disaster in India and occur every year. They have affected more than 370 million people, caused over 35,000 deaths, and resulted in damages exceeding 100 billion USD. The floods of 2014 and 2020 were the costliest, each causing damage exceeding 30 billion USD (EM-DAT).

Storms, mostly reported in the Bay of Bengal, are the second most frequent hazards in India. They occurred in all years except 2004, affecting over 73 million people. Although common, storms caused only about half the economic damage of floods and resulted in fewer deaths, mainly due to better forecasting and preventive measures taken by the government. Moreover, over the last six years, there has been a 400% increase in lightning incidents associated with storms.

Extreme temperatures, though less economically devastating, have had a high mortality rate of over 40 percent compared with the number of people affected. Droughts, on the other hand, have impacted the most to over 680 million yet have caused relatively fewer deaths and lower direct economic damage (EM-DAT).

Figure 1: Overview of hazards and corresponding disaster trends in India from 2000 to 2024 (Source: EM-DAT).

The disaster risks are further intensifying due to climate change. Rising sea levels, frequent high-intensity storms, extreme temperatures, and erratic rainfall patterns are increasing both the intensity and frequency of natural hazards in India, causing more destruction. A study by Picciariello, A., et al. (2021) stated that climate change could reduce India’s GDP by 2.6% if the increase in the global temperature remains below 2°C, while any increase of up to 4°C can decline the economy by up to 13.4% by the year 2100. Lower-income and marginalized communities are disproportionately at the forefront of the disaster, with many engaged in agriculture or odd jobs, directly impacting their daily lives, forcing them to migrate and causing a significant impact on their livelihoods.

Disaster Displacement

According to IDMC, between 2008 and 2024, floods and storms were the two major drivers of displacement in India, displacing over 45 million and 15 million people, respectively. The EM-DAT records reveal a different pattern when comparing damages to displacement. While the cost of damages due to floods and storms has steadily increased, the number of people displaced has fluctuated over the years.

The cost of damage increased primarily due to rapid urban growth and economic development, as concentrated assets in cities mean that even moderate floods can cause substantial financial losses. Urbanisation plays a dual role: it amplifies damages due to the presence of more “damageable” infrastructure, and on the other hand, it also reduces the displacement by enabling relatively resilient housing, faster disaster response, and better services, although informal settlements remain highly vulnerable (Hussainzad, E. A., & Gou, Z..,2024). Furthermore, 50% of India’s public infrastructure remains unprepared for disaster management, stemming from unplanned urbanisation, a changing climate, and development in high-risk zones.

Assurances through Insurance and Innovative Financing

With rising damages, financial protection becomes essential, as only 5% of damages in India are covered by insurance for natural hazards, compared to 40% in the USA. Disaster risk insurance now plays a crucial role in mitigating disaster risks by safeguarding assets and livelihoods in a changing climate.

India’s National Disaster Response Fund (NDRF), established under the Disaster Management Act, 2005, which acts as a supplement to the State Disaster Response Fund (SDRF), financially supports relief, response, and rehabilitation of the damages due to natural hazards. However, since this is a post-disaster fund rather than an insurance, it can take a significant amount of time to reach beneficiaries, which can impact timely recovery.

Considering the imminent rise in frequency and intensity of natural hazards and the corresponding potential for disaster and damage, financing disaster-related insurance can become a key to a faster recovery. According to the report “Leading the Path to Insurance for All” published by the Insurance Brokers Association of India (IBAI), only one in two and two in five are covered for life insurance and health insurance, respectively. Therefore, considering the scale on which people in India take up life and health insurance, the willingness to invest in insurance against disaster damage looks doubtful.

Nevertheless, there are several cases where insurance solutions have played a crucial role in recovery in other parts of the world, which can also be implemented in India.

- The community-based flood management and insurance in Bangladesh was initiated to protect vulnerable populations by linking it with microfinance initiatives to enhance its accessibility. In the Caribbean, a similar insurance scheme that pools the finances and shares risks across regions can prevent any single community from bearing the entire burden of a disaster, especially for low-income households. At the same time, insurance can encourage damage reduction by linking insurance premiums to risk mitigation measures, such as elevated housing or adhering to rules for flood-risk zones.

- Parametric Insurance, which provides pre-specified payouts in case of an extreme event in a short duration of time, without much administrative hassle. Nagaland, which has initiated such insurance, can serve as a good model for other Indian states to introduce similar insurance.

- Another example is the National Flood Insurance Program (NFIP) of the Federal Emergency Management Agency (FEMA), USA. NFIP is a partnership between the federal government, private insurance companies, lending institutions, and state and local officials, which is designed to provide affordable insurance to the communities and businesses in flood-prone areas. It not only offers direct coverage but also incentivises communities to adopt floodplain management regulations in exchange for access to insurance. While NFIP has faced challenges such as underpricing risk and mounting debts after large disasters like Hurricane Katrina and Hurricane Harvey, it has nonetheless provided a critical financial safety net to millions of households.

From rapidly urbanising areas to the increasing cost of damages, safeguards for critical infrastructure to reduce economic losses for public infrastructure also require innovative financing mechanisms to alleviate the burden on governments. Instruments like Catastrophic Bonds, a type of debt instrument, can be used to transfer catastrophic risks to capital markets. This can enable the government to receive prompt payouts in the event of extreme events, thereby reducing the burden on the exchequer to release funds.

Final Thoughts

In the technologically advanced 21st century, some nations have advanced resources, such as Early Warning Systems (EWS), weather forecasting tools, and robust financial mechanisms, that play a crucial role in forecasting and assessing hazards. However, in an era of exacerbating disaster risk, predicting hazards is only the first step; translating predictions into timely action that saves lives, reduces displacement, limits economic losses, and boosts post-disaster recovery remains the true challenge.

For India, the path forward requires a decisive shift from ex-post financing to ex-ante financing, which integrates risk reduction into planning, budgeting, and development. This means strengthening early warning systems, building and updating robust disaster action plans at state and district levels, and investing in public awareness and community mobilisation to ensure that alerts translate into effective local responses.

Resilience also depends on reducing the structural drivers of vulnerability. Investing in flood-control infrastructure, improving river-basin management, preventing settlements in high-risk floodplains, and expanding and maintaining urban drainage systems can help mitigate the impact of recurring floods. At the same time, policies must strengthen agricultural resilience by promoting the adoption of flood-resistant crops and encouraging community-based water management practices. To protect vulnerable populations, social protection measures, such as the broader rollout of disaster-risk insurance, crop insurance, and emergency food distribution systems, are crucial for fast recovery and in mitigating the long-term socio-economic consequences.

Although India does not have a dedicated national insurance framework for disasters caused by natural hazards, the government already has several insurance initiatives in place. These include: (1) the Pradhan Mantri Garib Kalyan Package, introduced in March 2020 in response to the COVID-19 pandemic, which provided comprehensive personal accident insurance for healthcare workers; (2) the Pradhan Mantri Fasal Bima Yojana, launched in 2016 and now the world’s largest technology-enabled crop insurance programme by number of insured farmers, offering protection against crop losses, including those due to disasters caused by natural hazards; and (3) low-cost insurance programmes such as the Pradhan Mantri Suraksha Bima Yojana, which offers personal accident coverage, and (4) the Pradhan Mantri Jeevan Bima Yojana, which provides life insurance in similar situations. The National Disaster Management Agency is putting extensive efforts to integrate these schemes, streamline disaster-related payouts, and create a consistent, forward-looking system to insure against the impacts of natural hazards. Despite this, there is still no statutory or executive mandate requiring comparable coverage for people affected by floods, earthquakes, or other catastrophes, leaving large segments of the population without protection.

At the same time, India has begun to see the gradual emergence of parametric insurance as a complementary tool for disaster risk financing. Unlike traditional indemnity-based products, parametric covers offer swift, predefined payouts triggered by measurable parameters, such as wind speed, precipitation, or earthquake magnitude, thereby reducing delays and administrative burdens associated with claims. Globally, parametric insurance models have been successful in enhancing financial resilience. Some prominent examples include the Coastal Zone Management Trust, Caribbean Catastrophe Risk Insurance Facility (CCRIF), Pacific Catastrophe Risk Insurance Company (PCRIC), and the Australia Parametric Cyclone Cover. As these models mature, they hold the potential to supplement existing government schemes and expand the financial resilience of communities affected by natural catastrophes.

Although several case studies have demonstrated the effectiveness of parametric insurance in limited regions of India (e.g., Nagaland), scaling these models nationwide remains challenging due to diverse climatic patterns, disaster risks, and varying levels of market readiness. A pragmatic way forward could be to develop a hybrid insurance framework that integrates the extensive outreach and administrative capacity of existing Pradhan Mantri schemes with index-based parametric products tailored to specific risks. This way, the speed and transparency of parametric triggers could be combined with the scale and subsidy mechanism of government programs, allowing wider adoption of insurance against disasters caused by natural hazards.

Another promising approach is to leverage India’s extensive network of microfinance institutions and Self Help Groups (SHGs). India has one of the world’s largest grassroot coverage of SHGs, with over 12 million such groups and more than 500 million Pradhan Mantri Jan Dhan Yojana (PMJDY) bank accounts. Notably, over 66.76% of PMJDY account holders have accident insurance and 31% with life insurance indicating relatively high penetration of low-cost social security insurance.

However, despite this wide outreach and strong community presence of SHGs, there is almost no systematic insurance coverage for disasters caused by natural hazards losses. By designing simple and affordable disaster risk insurance products which can be delivered through SHGs by linking enrollment and premium collection via PMJDY accounts of the members. This can create a community based insurance model which can increase the penetration of the disaster risk insurance, significantly reduce risk, enhance trust, improve affordability, and over the time build a culture of risk protection that encourages households to insure themselves for other insurance products.

Formulating and implementing policies or financial schemes can be a significant challenge in India due to complex socio-economic and political dynamics. These factors present both challenges and opportunities as the country navigates its current stage of development. One path leads to a future of a growing number of disasters, where millions are forced from their homes each year, and development gains are repeatedly wiped out. The other path demands bold action: to integrate disaster risk reduction and financial protection into the National Level Programme, thereby intertwining them with the very fabric of national development. Choosing the latter is not optional – it is the only way to secure a future where resilience becomes the foundation of prosperity.