Abstract

Due to the current global warming and climate change trends, there is a need to shift to cleaner forms of energy. Green hydrogen is a clean and sustainable alternative to other forms of hydrogen fuel. With India’s commitments to scale up on green hydrogen production, use, and export, there is a significant opportunity for the nation to become a leader in the arena of green hydrogen. This paper examines the key challenges and avenues for India to adopt green hydrogen, including infrastructure requirements, financing, and other prerequisites. The paper also discusses the short-term environmental and economic costs of transitioning various sectors of the economy such as transport and energy to sectors that can function on green hydrogen. The paper concludes with a brief discussion of the latest union budget provisions pertaining to the energy sector and green hydrogen, and suggests a way forward for the transition. Keywords: Green hydrogen, green energy, energy efficiency, GHG emissions, transition to green hydrogen.

What Global Significance of Green Hydrogen

Due to imminent global warming and declining environmental trends, the current energy ecosystem of the world is facing several challenges and requires urgent transformation. An increasing trend of renewable energy use can be seen globally, paving the way for innovations and further investment into cleaner sources of energy. This trend has emerged strongly in the transport sector, with increasing prevalence of renewable transport options through electric vehicles and other fuel-friendly options.

Derived from one of the most abundant and ubiquitous elements in nature, green hydrogen is a clean, efficient, and green fuel. It can be produced using renewable and non-renewable energy sources and technological inputs, all of which have different greenhouse gas emissions (The Economist, 2021). However, most of the hydrogen presently in use is derived using fossil fuels. Hydrogen generated using coal is known as grey hydrogen, whereas hydrogen generated using natural gas is known as brown hydrogen. These forms of hydrogen release carbon dioxide on combustion. Green hydrogen, on the other hand, produces no carbon emissions. It is generated through the process of electrolysis, which relates to using electricity to split water into hydrogen and oxygen. This electricity is generated using renewable sources of energy such as solar energy and wind energy, and hence, the hydrogen fuel which is extracted from this process is called Green Hydrogen (Chauhan, 2022).

Hydrogen and its derivatives can play an important role in reducing emissions in hard to abate sectors such as heavy industries, shipping, transportation, and aviation. In the year 2021-2022, the consensus towards hydrogen as a fuel remained positive, with nine countries having 30% of global energy sector emissions drafting concrete plans for integrating hydrogen into the energy ecosystem (IEA, 2022). The demand for hydrogen also grew for new applications like fuel cells for electrical vehicles – particularly in heavy trucks in China. Furthermore, when it comes to the transportation sector, the world’s first fleet of hydrogen trains started operating in Germany. Various shipping companies have also committed to strategic partnerships to obtain hydrogen derivatives in the short term (ibid.). Unfortunately, the majority of current hydrogen production results in grey hydrogen as a product, since these production practices use coal, natural gas, and other cheap production methods for electrolysis which are harmful for the environment. The production of hydrogen used in the petrochemical industries and the chemical sectors itself is responsible for more than 900 metric tonnes of carbon dioxide annually (ibid.).

Switching to green hydrogen use in such sectors can be beneficial since a transition to green hydrogen use won’t present severe technological challenges, since only the source of hydrogen changes.

Global Policies for the Development and Implementation of Green Hydrogen

China produces and consumes the most hydrogen. Annually, the hydrogen expenditure of China stands at more than 24 million tonnes. Most of China’s hydrogen consumption comes from grey hydrogen, but a number of projects using green hydrogen have been set up since 2019. China issued its first hydrogen roadmap in 2016, and the country’s five-year plan recognises hydrogen as an industry for the future. While China has no national strategy in place for hydrogen development, 16 provinces and cities in the country feature hydrogen in their energy development plans (Wood, 2022).

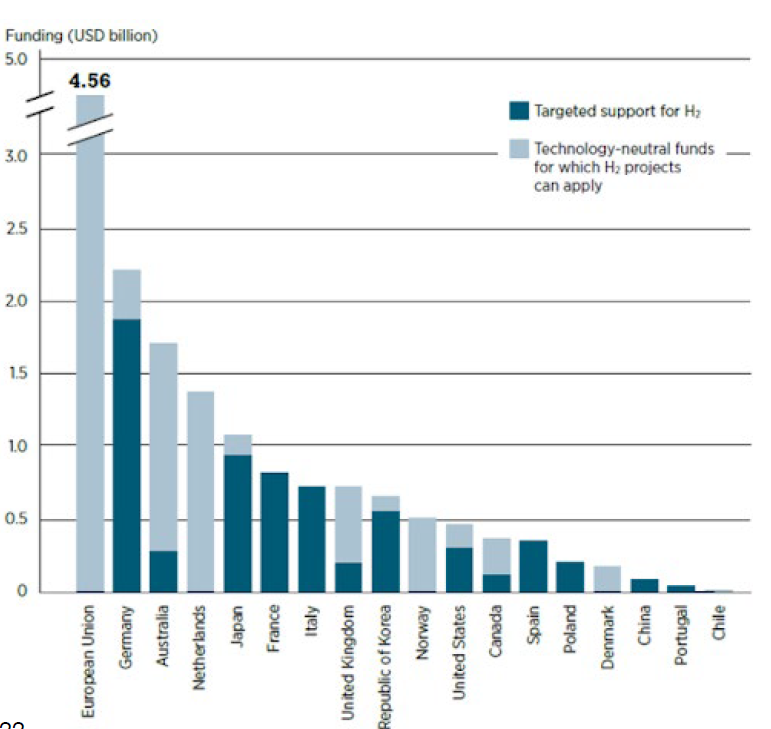

Hydrogen has received due recognition in the European Union [EU] as well. The EU has realised the potential of hydrogen in achieving goals set in the European Green Deal. The EU’s present energy strategy heavily focuses on emissions-free green hydrogen production, with the goal of installing 40 gigawatts of green hydrogen capacity by 2030 (ibid.). The European Clean Hydrogen Alliance was also launched in the EU to support and invest into large scale setting up of hydrogen projects. Within the EU, several nations have also made commitments to become large scale hydrogen importers and exporters. Furthermore, the funding potential for hydrogen based projects in the EU stands at a whopping $4.56 billion (ibid.).

Source: Wood, 2022, Potential funding opportunities for hydrogen projects in the EU.

Infrastructure Challenges to Transitioning towards a Green Hydrogen Economy in India

While a transition towards a green economy is required to counteract the current global warming trends and climate change, there are several challenges that need to be addressed before India can fully transition towards a green hydrogen based economy.

The main infrastructural challenges that India faces in the transition to a green hydrogen economy and production of green hydrogen are – the lack of adequate electrolyser capacity, and storage and supply chain issues.

1. Lack of Adequate Electrolyser Capacity

Generally, to produce one million tonnes of green hydrogen, an electrolyser capacity of 11-13 gigawatts is required (The Times of India, 2023). According to the goals of the NGHM, if India expects to produce 5 million metric tonnes of green hydrogen per annum, it would require an electrolyser capacity between 55-65 gigawatts. In contrast, India is only expected to achieve 8 gigawatts of electrolyser capacity by 2025 (ibid.). Even though there are efforts to overcome this lack of electrolyser capacity through the SIGHT program, the gap is large and would require considerable efforts to close. Furthermore, the most efficient electrolysers currently in operation consume around 50 kWh of electricity to produce 1 kg of hydrogen. If India aims to achieve 5 million tonnes of green hydrogen production by electrolysis, India would require 250 billion kWh (around 115 gw) of electricity supply from renewable energy sources. In contrast, as of February 2022, India has a capacity of 106 gw of renewable energy, from all viable sources (Kumar, 2023). This is an important factor to consider, since almost all of the installed renewable energy capacity would have to be directed towards generating green hydrogen, if the installed capacity of renewable energy sources is not increased significantly.

2. Storage and Supply Chain Challenges

The whole supply chain of producing green hydrogen is very complex. It includes usage of large amounts of renewable energy, transportation, distribution, storage, and handling. Additionally, due to the physical properties of green hydrogen, it requires additional infrastructure for safe handling. Hydrogen is a very light gas, and occupies a much larger volume than other gases under normal atmospheric pressure. Storing 1 kilogram of hydrogen requires a storage capacity of 11 cubic metres. It is also possible to store hydrogen in liquid form, but the process is very complex and expensive. Barring the storage challenges, hydrogen in its gaseous state is odourless, which makes detection of leaks very difficult (Storing Hydrogen | Air Liquide Energies, n.d.). To facilitate the storage of green hydrogen, the government of India has commissioned the construction of bunkers for storage, however the specifications and the technical provisions of these facilities are not confirmed (ET EnergyWorld, 2022).

Assuming that adequate investments are made to meet the electrolyser capacity requirements, renewable energy capacity, and storage and infrastructure prerequisites, the development of these facilities and infrastructure will have an explicit increase in short term emissions.

An Overview of the Short-term Emissions of the Transition

The International Renewable Energy Agency has raised concerns about the availability and the feasibility of the raw materials that go into the production of electrolysers. Alkaline electrolysers that are the most prevalent today are reliant on metals such as steel and nickel, but these electrolysers have a higher area footprint. The more compact polymer-electrolyte membrane and solid-oxide electrolysers, which can also support different sources of renewable energy however, require platinum and iridium for manufacturing ( Collins, 2022; Koundal, 2021). Platinum and iridium are among the most emissions-heavy metals in the world. Presently, no substitute is available for iridium use in electrolysers. Most of the platinum and iridium reserves in the world are found in South Africa, which means that the metals must be imported to India, levying additional environmental and economic costs. In 2021 itself, India imported 10.59 tonnes of platinum (Jadhav & Ahmed, 2022).

Furthermore, there is a significant emissions cost associated with green hydrogen infrastructure. As mentioned earlier, to meet the hydrogen generation goals, India would need to scale up green hydrogen production exponentially, requiring hydrogen plants, electrolysers, storage facilities, transportation facilities such as pipelines, roads, vehicles, etc., which will have emissions of their own. And these emissions will be directly proportional to the scale of green hydrogen expansion, and can prove to be environmentally and socially harmful in the short run.

An additional consideration when it comes to green hydrogen production is the water consumption. The most efficient alkaline electrolysers in use presently use 10 litres of fresh water to produce 1 kilogram of hydrogen. Therefore, 50 billion litres of freshwater would be required annually to meet India’s goal of producing 5 million metric tons of green hydrogen per year (Kumar, 2023). However, it is predicted that by 2030, the demand for water in India will be twice as much as the supply (TERI, n.d.). Adding on the water requirement for green hydrogen production into this projection could mean that water scarcity could potentially affect millions of people, along with several other industries and economic activities.

Other Barriers to Green Hydrogen Production in India

In addition to short term emissions, there are a few obvious barriers that need to be considered. These barriers include waste management, cost management, and infrastructure management. Waste management is one of the largest global challenges when it comes to adopting green hydrogen. Setting up of infrastructure for green hydrogen production will involve construction and resource intensive operations which generate high amounts of solid waste. Historically, solid waste management has been a problem area for many urban local bodies in India due to industrialisation and economic growth, both of which have increased solid waste generation. In spite of rapid industrialisation, solid waste management mechanisms have not evolved in the country. More than 90% of solid waste is dumped rather than properly landfilled or processed (Kumar et al., 2017). The current solid waste management mechanisms are highly inefficient and outdated, and can have severe consequences for public health, the environment, and the economy if not addressed urgently.

One of the biggest barriers to the large-scale adoption of green hydrogen would be the high costs associated with the fuel. The production process of hydrogen is energy intensive, making the product fairly expensive (Eh et al., 2022). Even though technological advancements can help address the end-user costs of green hydrogen, it is also imperative to generate adequate end-user demand which can lower the production cost of hydrogen by economies of scale.

Besides the short term emissions and other related challenges of setting up green hydrogen infrastructure, there is an additional environmental cost to be borne in order to transition certain industries and the transport sector to properly function using green hydrogen as a fuel.

The Environmental and Economic Cost of Revamping Industries and Transport

One of the most polluting segments of the economy is transportation. The number of registered private vehicles in Delhi in 2021 reached 3.31 million units, with the total number of vehicles operating in India being around 295 million (Statista, 2023). India has the third largest road network in the world, and a majority of people prefer road travel. Aside from public commute, industrial movement of goods in India has also been on a rise, with over two billion tonnes of freight being transported through roads in 2017 (Statista, 2022). With the global focus shifting towards sustainable modes of transport like EVs and fuel cell vehicles, the transport sector should be one of the top priorities when it comes to incorporating green hydrogen in the economy.

According to research by John Heywood, a professor of mechanical engineering, retrofitting traditional automobile engines to support hydrogen as a fuel can be done, but the process is far too complicated and costly to be viable (Sutton, 2010). The only places where retrofitting traditional engines is viable is long haul trucks and large diesel and gas vehicles like buses (ibid). This presents the problem of either spending money on retrofitting older engines, or replacing the on-ground vehicles with fuel cell vehicles. Manufacturing new vehicles to replace the ones already on the road, or even gearing towards replacing 50% of the vehicles will be both environmentally and economically costly, and might also receive negative backlash from the general public. Manufacturing a new automobile releases 5.6 tonnes of carbon dioxide on average (Campbell, 2022). Taking into account the number of vehicles on the road in India, replacing the vehicles on road will lead to a considerable increase in carbon dioxide emissions.

When it comes to industries, green hydrogen will mostly be used in heavy industries such as oil refineries, fertiliser plants, chemicals, cement, ammonia, and steel and iron (Pandey, 2022). However, calculating the exact environmental and economic costs of transitioning from traditional thermal energy to green hydrogen use would require extensive data and primary research which is presently not available. A swift transition to hydrogen in hard-to-abate industries1 is highly unlikely in India. However, in a carbon constrained economy, green hydrogen based steel production could help in building domestic demand for hydrogen and provide employment to more than 1.6 million people by 2050 in the hydrogen supply chain. The ammonia production industry could also benefit from transitioning to green hydrogen, which will help in cutting down on natural gas use and also generate jobs along the supply chain (Biswas et al., 2019).

Recently, India has set targets for some industries to adopt green hydrogen to generate demand for the fuel. The country has set a target for the Shipping Corp of India, the largest fleet operator to retrofit at least two vessels to run on green hydrogen by 2027. Additionally, all state-run oil and gas companies that charter more than 40 vessels for fuel transport will mandatorily need to hire one ship operating on green hydrogen every year from 2027-2030 (Reuters, 2023). Such target-based measures can prove to be helpful in the long run if they are scaled up according to the built capacity and the availability of resources and investment in the hydrogen ecosystem.

Addressing the Challenges

Addressing the challenges to adequately transition to a green hydrogen based economy involves innovation, scaling up technology, generating domestic demand, and regulatory measures. India’s R&D expenditure compared to GDP share stands amongst the lowest in the world (Biswas et al., 2019). In 2022, India spent only 0.65% of its GDP on R&D (Statista, 2023b). The low levels of innovation and research has led to the manufacturing process being stagnant and old-fashioned. The country needs to start investing more into R&D through pilot projects and collaborations with universities and even foreign bodies. A public-private partnership in R&D can also help cut down risks associated with research and testing out new technologies. Furthermore, developing consortiums with several key research institutions domestically and internationally can also help in advancing R&D in the country, which will in turn make manufacturing processes efficient and less polluting, while paving the way for adoption of green hydrogen (ibid.).

Another challenge to address is the price of renewable energy in India. For large scale green hydrogen production, it is important to make renewable and clean energy cheaper and economically favourable when compared to conventional energy sources such as coal and natural gas. Private sector participation in renewable energy supply chains and production can lead to healthy competition in the ecosystem, leading to a positive shift in pricing. Furthermore, enforcement of emissions standards in India has not been done properly. Energy prices currently do not reflect the actual environmental cost and health impact, thereby making renewable energy more expensive. Holding industries and pollutants accountable for their energy use through conventional polluting sources can further help in reducing costs of renewable, clean energy sources. A revised set of emissions standards for energy intensive industries can help ensure that newer facilities are built in an energy efficient manner, and do not have a transition cost (Biswas et al., 2019).

When it comes to adoption of clean energy, consumers also have a strong influence on manufacturing processes and use of sustainable raw material. Governments across the world are leveraging consumers to create a domestic market for green energy. In India, the Bureau of Energy Efficiency has been running a Star Labelling Programme which promotes consumer awareness for electric appliances. A similar sort of programme could be started to increase awareness about emissions footprint for a product’s life cycle, informing customers about life cycle emissions and energy use of the product (Biswas et al., 2019).

Following these measures, hard-to-abate sectors have the possibility to be decarbonised using green hydrogen.

What Union Budget 2023 Considerations

To further the green hydrogen agenda in India, the union budget made some much needed contribution to the Green Hydrogen Mission. As mentioned earlier, Nirmala Sitharaman, the finance minister of India announced an initial outlay of Rs. 19,700 crores for the mission. Additionally, the government has allotted Rs. 297 crore for the first year of the mission (Kumar, 2023). There are also plans to offer incentives to investors and support pilot projects for green hydrogen.

However, it still remains to be seen how this initial investment and the outlay in the budget is used in India to increase green hydrogen production and demand. Hemant Mallya, Fellow at the Council on Energy, Environment and Water (CEEW) commented “Till now there is not much clarity from the budget besides its total allocation and the overall target of the mission. It is crucial to see how the budget is utilised…it is a fast-moving industry and we have witnessed a lot of developments in the last six months. So, if we can capture the domestic supply chain market early, this can give us an added advantage” (ibid.).

Thus, even with an enormous budget allocation into green hydrogen, it is imperative to draw up a detailed roadmap for development of infrastructure and other related facilities for green hydrogen production.

Concluding Comments

With India’s nationally determined contributions towards fighting climate change being heavily focused around renewable energy and now green hydrogen, it is important to take account of the country’s current standing and capabilities. When it comes to infrastructure requirements and inputs for the aimed green hydrogen production, it is seen that India is lagging behind in electrolyser capacity, and the water requirement for producing 5 million metric tonnes of hydrogen is hard to achieve annually. India must revisit its goals for green hydrogen production and phasing out the use of coal and other polluting sources of energy – being a developing country, the nation is bound to emit a certain threshold of emissions for a short period of time, which will in turn enable greener transitions in future.