Across the globe, around a hundred million barrels of oil are in demand each day [1]. It was estimated that in 2020, this number will increase by 825,000. However, in sharp contrast, following the spread of the Novel Coronavirus, the oil demand has instead fallen by 90,000 barrels per day [2]. In fact, global oil demand may continue to fall by about 30 million barrels per day solely in response to the COVID-19 pandemic.

Even in the face of downward spiralling demand, the production of oil has continued at more or less the same pace, resulting in a shortage of storage facilities; forcing prices to fall in the hope of attracting buyers. But, the industry faced the biggest hit of the season last week, when the price of a barrel of crude oil hit negative, falling below 0 USD [3].

WHAT IS CAUSING THE DECLINE IN OIL PRICES?

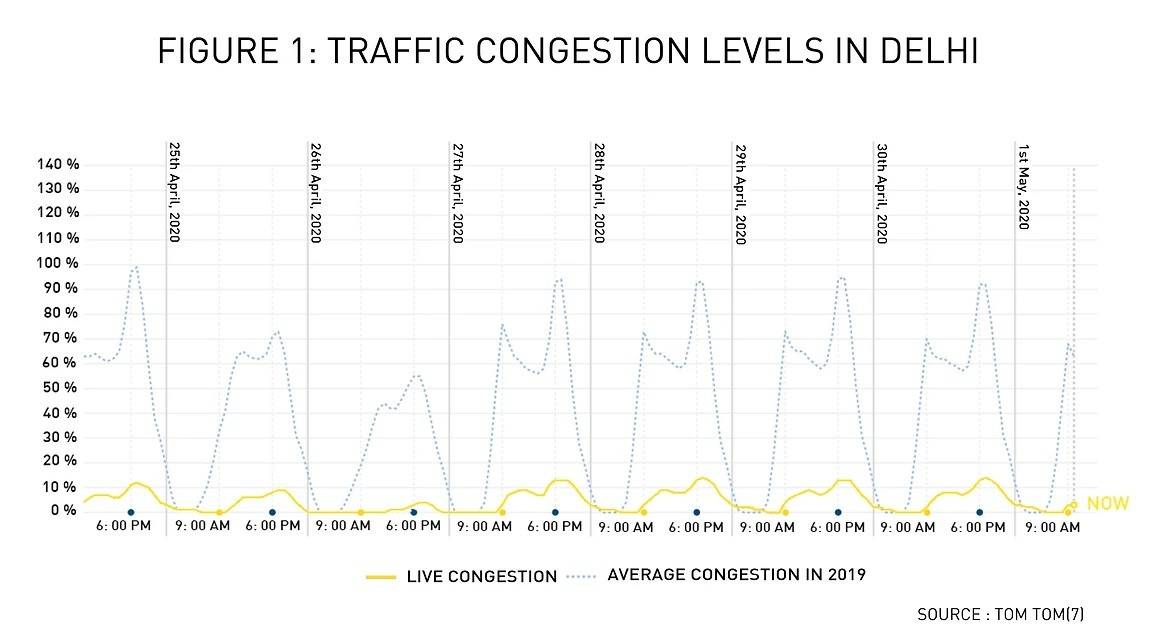

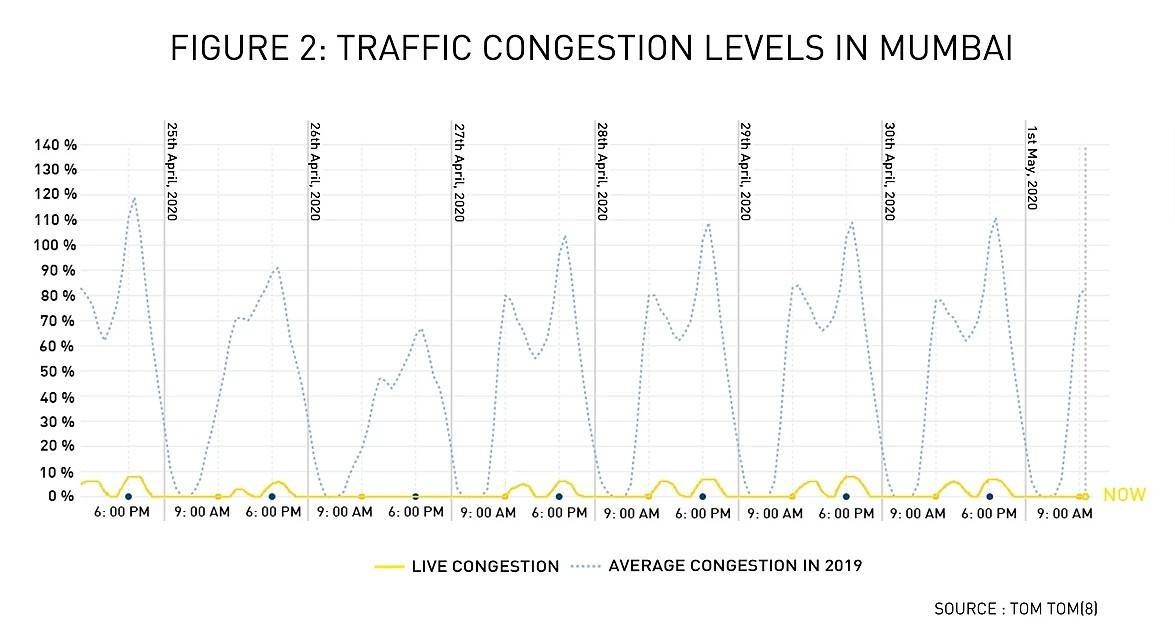

Decreased transport fuel consumption due to significantly lesser movement of people and goods is the single biggest reason driving oil prices towards zero. As people worldwide practice self-isolation, traffic on roads and highways has reduced dramatically in recent weeks. Government reports in the United Kingdom confirmed that road travel has decreased by over 70%; while in certain cities in the United States traffic is moving 50-70% faster [4] [5]. In Mumbai and New Delhi, both ranking amongst the 10 most congested cities in the world, movement on roads has slowed down significantly, coming to a near standstill (Figure 1 and 2). As all commercial operations within the aviation industry also remain suspended, it is being projected that air passenger traffic will register a 30% negative growth, impacting crude oil consumption heavily in the year to come [6].

Even though the demand for diesel was set to gradually decline over the decade owing to increasing transitions to cleaner energy sources and electric vehicle technologies, the industry was far from prepared for a sudden plummet.

However, the Novel Coronavirus pandemic is not the only cause behind the recent oil market trends. The last month also saw weak attempts at coordination between Russia and Saudi Arabia, both major oil-producing countries, to cut their production levels in response to decline in consumption due to the COVID crisis [9]. Even though OPEC and its allies have now entered into an agreement whereby they have committed to cut almost 10 million barrels per day of crude oil production in the coming months of May and June, how quickly such a cut will come into effect remains debatable. Putting a pause on pumping out oil is a costly affair, just as building and maintaining infrastructure to hold oil are heavily capital-intensive tasks. Producers are not keen on taking this step, fearing that a sudden improvement in the current situation will in turn lead to them losing market shares. Thus, several oil companies need to continue production simply to stay afloat, even without clarity of who they are producing for.

INDIA: DEMAND AND IMPORT

Even though the global consumption of oil has shown a declining trend in relation to the world GDP over the past couple of decades, India has remained a country with high consumption of and dependence on oil. India spent 112 billion USD on importing crude oil in 2018-2019 to meet over 80% of our oil needs, indicating quite evidently that our domestic oil production is dismal [10]. It is being anticipated that the current oil prices will play to India’s advantage, by cutting down our import bill for the current financial year by almost 10% and helping ease the burden of fiscal deficit. Further, a dollar worth’s decrease in the crude oil prices has the potential to save India about INR 2,900 crores [11].

However, the potential of short-term benefits for India from the COVID-disruption in the oil and gas industry needs to be examined more closely, even as it remains unclear whether these benefits will spill over to the long term.

At the outset, India’s capacity to store oil lags behind most other Asian countries. Combining the capacities at Visakhapatnam, Mangalore and Padur, Indian can hold about 37 million barrels of oil in reserve, enough to cover the country for a mere 9 days in the event of a crisis. In comparison, China, Japan and South Korea have a capacity to store 550, 528 and 214 million barrels respectively. Nonetheless, our strategic reserves are only about half full, leaving scope for India to stockpile while prices are low.

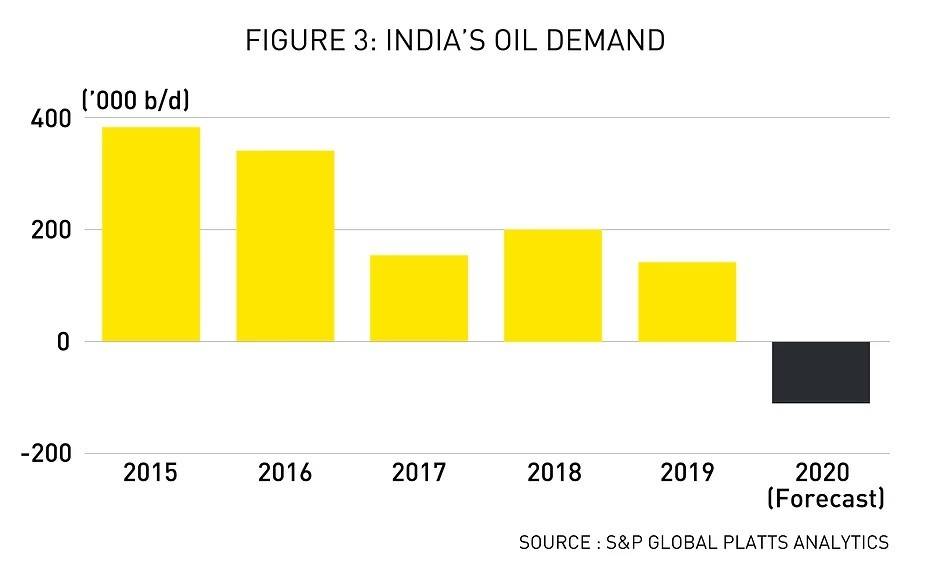

However, as it remains unclear how long the lockdown will extend, both domestically and internationally, continued fall in demand might soon counter the gains India might reap from declined oil costs (Figure 3). In this context, our import of crude oil has already reduced by half in volume and thus, the benefits from lower oil prices might only amount to a minimal 0.1 to 0.2% of our GDP [12].

Furthermore, the rupee continues to be weak against the dollar, as even in a scenario replete with uncertainties, the confidence of consumers in the dollar remains high. An unfavourable exchange rate will definitely offset any reduction in cost of import. Thus, it remains crucial for India to remain alert for inflationary trends in the market and protect the position of the rupee as and when the lockdown is lifted; alongside consciously determining the pace of the same.

Moreover, it is unlikely that price cuts in raw crude oil globally will be passed over to the consumers, measured in terms of the retail cost of petroleum products in India. The benefits from lower oil prices might be used by the government to make up for the significant decline in its revenue amidst the lockdown. In addition, even in the case that the final price of petrol, diesel and kerosene declines, the purchasing power of an average Indian consumer might not increase significantly. The fear of an unstable economy will push consumers towards safer investments, if they choose to invest at all. Thus, claims of India’s potential to exploit the near zero cost of futures trading in oil seem rushed and inflated.

Regardless, by all estimates, production is set to rise faster than demand in the case of oil in the next five years. As per the International Energy Agency, between 2019 and 2025, demand will grow at almost 1 million barrels a day annually, however, global oil production capacity will grow at a staggering 5.9 million barrels a day [13]. Thus, how quickly policymakers re-adjust to the post-corona normal will be crucial in determining the recovery of all economic activity.